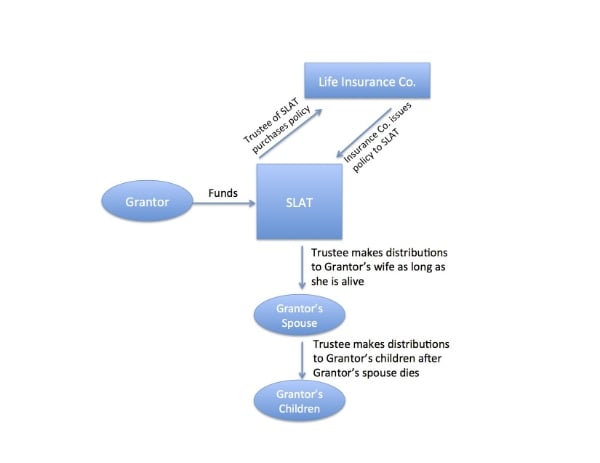

The Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that holds a life insurance policy on the grantor’s life. The SLAT has two tiers of beneficiaries. The initial beneficiary is the grantor’s spouse; the secondary beneficiary is the grantor’s child[ren] (or whomever or whatever the grantor chooses). The grantor is not a beneficiary of the SLAT. As long as Grantor’s spouse is alive, she is the only beneficiary. After Grantor’s spouse dies, the secondary beneficiaries receive distributions of trust property as dictated by the grantor. If Grantor’s spouse predeceases Grantor, the trust assets and the future death benefit will be held in trust for the second tier of beneficiaries.

A SLAT can be funded with a lump sum or annual payments using the grantor’s gift tax exclusion ($14,000 per person each year). An ideal arrangement for many couples would be to have the trustee of the SLAT purchase a whole life insurance policy. Over the years, the cash value of the policy accumulates.

The first benefit of a SLAT is that Grantor’s spouse has access to funds if she needs them. As the initial beneficiary, if Grantor’s spouse needs money before Grantor dies, she can receive distributions from the cash buildup in the policy owned by the SLAT. When Grantor dies, the death benefit pays out to the trust, thereby giving her access to the death benefit if she needs it. If she doesn’t need the death benefits, they are held in trust for the second tier of beneficiaries while being kept out of her taxable estate.

The second benefit is that the life insurance policy is not included in Grantor’s taxable estate. The SLAT is structured in a way that gives Grantor no incidents of ownership over the policy, thereby excluding it from his taxable estate. Thus, Grantor is (potentially) able to move a significant amount of money to his children free of estate tax.

The third benefit of a SLAT is that Grantor can benefit indirectly from the SLAT. Even though the grantor is not a beneficiary of the trust, the grantor can no doubt benefit from trust distributions to his spouse. However, if Grantor’s Spouse predeceases or divorces Grantor, then Grantor receives no such indirect benefit.

The final benefit of a SLAT is that it offers tremendous asset protection. The cash buildup of the life insurance policy in the SLAT and the policy’s death proceeds are protected from creditors of both Grantor, Grantor’s spouse, and the beneficiaries.

Example

Grantor has three children. He funds the SLAT with his annual exclusion amount each year ($14,000x3children= $42,000 annually). The trustee purchases a whole life insurance policy. Twenty years later, these tax-free gifts total $840,000. Grantor’s spouse, as a beneficiary has access to the cash buildup if needed. When Grantor dies 25 years after settling the SLAT, the death benefit is $3,000,000, paid to the trust. Grantor’s spouse can access the death benefit if needed. Assuming she doesn’t access the death benefit, when she dies, the $3,000,000 is distributed to Grantor’s children. Thus, Grantor has effectively given his children $3,000,000 free of estate taxes, while providing funds (free from claims of creditors) for his spouse during her life.